The great transition to clean energy sources is in full swing. The International Energy Agency expects renewables to make up 80 percent of the world’s new energy capacity by 2030. An annual amount of 500 gigawatts (GW) of solar will be installed every year.

Within this fast-paced industry, several market conditions continue to redefine the way business is done. From geopolitics to supply & demand, today’s PV professional must keep tabs on subsidies and incentives, price volatility, new technology, and product lifecycle policies and standards.

Because all PV projects begin with solar panels, industry players across the supply chain should have a keen understanding of the issues that surround the module market.

Beyond new construction, the solar panel lifecycle from maintenance to reuse to recycling is a major facet of developing a circular economy within the solar industry. And although a secondary market to address lifecycle solutions is ramping up, still more awareness and funding are needed to create a robust downstream channel.

In this article, we examine three current solar panel market conditions that will likely continue through next year: (1) a massive increase in domestic manufacturing, (2) the rise of new cell technology, and (3) the state of reuse & recycling. In each section, we’ve included preliminary results from EnergyBin’s 3rd annual PV Module Price Index, which will be released in January 2024.

The world wants "Made in [Name Your Country]" solar panels

The first condition to consider is the massive increase in domestic manufacturing. In 2023, countries and private investors alike have stepped forward with huge amounts of funding for making polysilicon, ingots, wafers, cells, and modules.

Since 2020, governments have earmarked $1.3 trillion to support clean energy investment. Funds are driven by supply chain vulnerabilities, which were exacerbated during the height of the coronavirus pandemic. Although the pandemic was not the leading cause for such weaknesses, it was the spark many governments needed to launch initiatives to resolve issues. The primary issue has been to gain independence, or at least reduce dependency, from China.

But China is a full decade ahead of the rest of the world and will continue to retain its 80 percent market share in 2024. The country created industrial policies to support the solar PV manufacturing process, which has led to economies of scale. In 2021, total trade exports from China, including polysilicon, wafers, cells, and modules, exceeded $40 billion.

Going forward, China has no intention of slowing down. By August, the Photovoltaic Manufacturing Industry Specifications Conditions reported an 80 percent year-over-year increase in the production of polysilicon, wafers, cells, and modules.

The supply surplus has led to falling module prices through the second half of this year. By mid-November, mono PERC and TOPCon module prices hit the lowest levels in the industry’s history at $0.130/Wp and $0.140/Wp respectively.

Meanwhile, other countries are spearheading new policies to propel manufacturing at home. The United States is leading the charge with the passage of the Inflation Reduction Act (IRA) in 2022. The IRA amounts to 40 percent of all rich-country spending for clean energy initiatives, which comes to between $400 billion and $1 trillion over the next decade.

Additionally, private investors have announced over $100 billion for more than 50 new or expanded solar manufacturing facilities in the U.S. By 2026, the country’s annual production capacity should include 58 GW of modules (or 52 percent of the 112 GW of capacity planned by this target date as adjusted in November by Wood Mackenzie analysts).

Manufacturers have also committed to 43 GW of cells, and 20 GW of silicon ingots and wafers; although, it’s likely that only 50 percent of these announcements will be operational in light of the surplus as well as the time necessary to set up such facilities. By 2033, the capacity is expected to reach 669 GW with private investments totaling $565 billion.

The trend to boost “Made in [Name Your Country]” production is popular in other regions as well. In Europe, the EU’s Green Deal Industrial Plan has allocated €270 billion for net-zero initiatives in member states. India has launched its production-linked incentives (PLI) scheme, which pays manufacturers a sum for every unit produced. And Japan’s Green Transformation Policy has reserved 20 trillion yen for bonds over the next decade and expects over 150 trillion yen in public-private investments.

As countries ramp up production, several questions come to the foreground. How price sensitive will buyers be? Will at-home incentives to buyers be enough to justify spending more for domestic modules (compared to imports)? Will subsidies allow domestic manufacturers to compete with global prices? And at what point does manufacturing output become wasteful?

Regarding price, it’s expected that China will continue to win on the lowest price. Though some argue that quality is more of a factor over price, buyers will still consider price, especially when quality differences are minuscule.

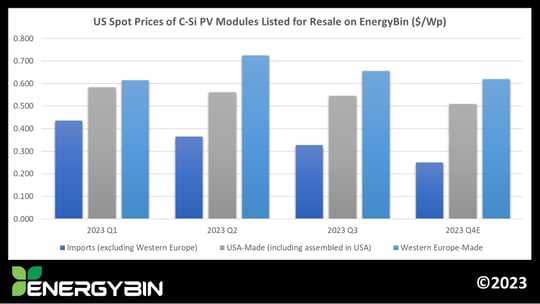

On EnergyBin, the average “Made in USA” module price per watt is ranging 40-45 percent higher than imports, excluding those from Western Europe. Brands manufactured in Western Europe, such as REC and Meyer Burger, are even higher in price than USA-made/assembled modules.

By December 31st, the price difference between imports and USA-made modules is expected to increase to 50 percent. As of late-November, the average price per watt of imported silicon modules (excluding those made in Western Europe) listed on EnergyBin is between $0.200 and $0.250. Likely, the $0.200 price per watt will hold steady or even decrease through December.

The gap between imports and USA-made module prices may very well close in the next several years. By June 2024, the tariff exemption on imports from Southeast Asia will expire. And as global manufacturers work to establish vertically integrated conglomerates, prices will stabilize.

For example, QCells has set up three manufacturing facilities in Georgia with an annual capacity to produce 8.4 GW of solar panels. The corporation is on track to achieve economies of scale thanks to a global network of three other manufacturing facilities in China, Malaysia, and South Korea and sales offices located in Europe, North America, Asia, Australia, South America, Africa, and the Middle East. QCells panels listed for sale on EnergyBin that are made in Georgia are currently posting at prices comparable to imports.

Subsidies from the IRA certainly helped QCells’ decision to expand from a capacity of 5.1 to 8.4 GW. Additionally, QCells will use the credits to make ingots, wafers, and cells. Furthermore, QCells has become the leading shareholder in REC Silicon, which has reopened a dormant polysilicon factory in Moses Lake, Washington. Yet, QCells first expanded into North America long before IRA subsidies were on the table. And the corporation is taking steps to outlast subsidies and establish a global presence for the long-term.

Meanwhile in Europe, the surplus is surging with an estimated 65 GW of stored solar panels in warehouses. Much of the supply was purchased earlier this year at higher prices. Europe is facing a significant influx of Chinese imports where it’s become no longer profitable for regional manufacturers. Latin America is also weakened by the surplus; although, analysts aren’t certain how much supply is stored in this region. And in the U.S., imports increased from $4 billion in 2022 to $10 billion through August 2023.

A major factor contributing to the surplus is the shortage of skilled laborers. To satisfy the need of operating 100 GW of solar module factories in the U.S., approximately 4,000 to 5,000 new employees must be hired. Finding and training qualified laborers to run these plants will be a challenge.

Additionally, employers are actively recruiting for new construction jobs. Roughly 176,000 employees currently work in the installation category. This number falls short of the 500,000 to 1.5 million people needed by 2035 to achieve the country’s energy transition goals.

Presently, finding qualified applicants is a challenge for 44 percent of employers. However, if the labor needed to construct new solar projects catches up to supply, manufacturers can raise prices and establish some level of price stability.

In any case, manufacturers will have to decide when to scale back to avoid wasteful production. This concern is especially imperative as the industry at-large moves from p-type to n-type cells and other innovations, like perovskite cells. Demand for higher efficiency panels is driving this change.

Moving from p-type to n-type solar cell technology

The second market condition – a rise of new cell technology – is inevitable as manufacturers achieve higher efficiencies. More manufacturers are making the switch because laboratory tests have determined that n-type cells are more efficient than p-type cells and are unaffected by light-induced degradation (LID).

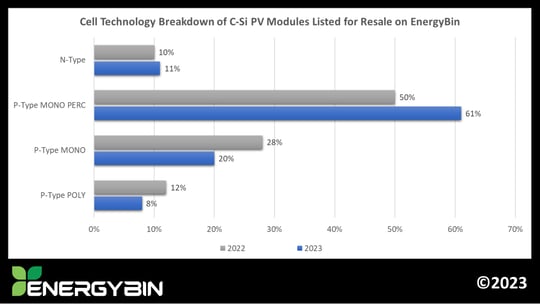

N-type cells come in three main technology forms: tunnel oxide passivated contact (TOPCon), heterojunction technology (HJT), and back contact (BC) panels. While HJT and BC outrank TOPCon on efficiency levels, TOPCon is gaining market share at a faster rate due to the ease of upgrading an existing PERC line with the tunneling passivation layer. TOPCon’s market share has increased from 8 percent last year to 21 percent this year, and is on track to dominate the market by the end of 2024.

This transition doesn’t mean that p-type PERC cells will disappear. In the 2022 PV Module Price Index, we stated that 90 percent of the modules listed for resale on EnergyBin were comprised of p-type cells (mono, mono PERC, and poly). This year, PERC modules continue to make up most sales listings while the shares of p-type mono and poly modules have decreased.

In the next ten years, however, the share of p-type PERC will decrease to about 10 percent while n-type TOPCon increases to 60 percent, according to the International Technology Roadmap for Photovoltaic (ITRPV). Following TOPCon, HJT will jump from 9 percent market share in 2023 to over 25 percent by 2033.

Additionally, perovskite cells, the latest innovation, are testing well for light absorption, charge-carrier mobilizers, and lifetimes. They rank highest in efficiency. For example, Sharp announced in November that its new silicon tandem solar cell achieved a power conversion efficiency of 33.66 percent. Although there’s potential for mass commercialization in the future, industry experts don’t anticipate a switch to perovskite taking place in the near term.

Overall, upgraded technology is a benefit for the solar industry. But it begs the questions about what to do with stored PERC module supply and how to handle maintenance of existing PV systems that were built with PERC technology.

Since higher module efficiencies make possible denser installations, which tends to lower the total cost of the system, many buyers have opted for n-type over p-type modules. In the latest Tracking the Sun report by the Lawrence Berkeley National Laboratory, the average U.S. installation in 2022 was built with modules ranging from 20 to 21.5 percent. This trend was consistent for residential, small non-residential, and large non-residential projects alike.

Therefore, the decision to resell stored PERC modules is becoming even more time sensitive. Sellers need to pay attention to what their primary buyers are demanding. If the demand isn’t there for PERC modules, then they need to resell them to other buyers in the secondary market. The longer legacy inventory is stored, the more it will negatively affect a seller’s bottom line.

Platforms like EnergyBin host pre-qualified volume buyers throughout the world. Depending on buyers’ needs, PERC modules sold at competitive prices may be appealing, particularly for maintenance applications or expanding existing arrays.

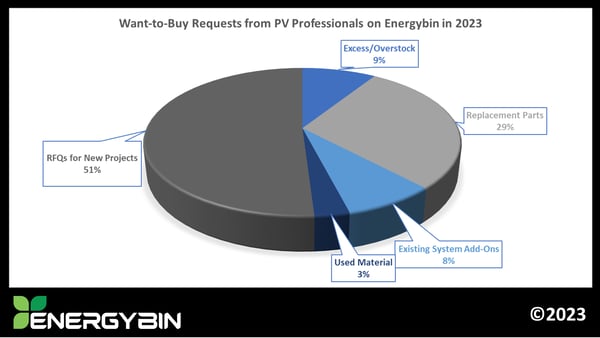

In the PV Hardware Trade Analysis H1 2023, over 45 percent of buyer requests were made for locating replacement parts, adding onto systems, or buying excess stock.

Oftentimes, modules that need replacement have been discontinued by manufacturers. The secondary market offers an alternative source for buying and selling PV hardware, whether that’s remarketing inventory that a seller’s primary buyers aren’t purchasing or finding replacement parts to maintain an existing system. It also provides a space to resell used solar panels as well as to connect with recycling partners for end-of-life material.

Where we're at with solar panel reuse and recycling solutions

The third market condition to watch in 2024 is the state of the reuse and recycling sectors. Over the past few years, people have begun to take an interest in alternatives to landfilling solar panels, but more players are needed to create a robust aftermarket infrastructure. Demand for secondhand solar panels must grow. And an increase in end-of-life solar panel supply is necessary for the recycling sector to achieve economies of scale.

The volume is coming. The International Renewable Energy Agency (IRENA) predicts cumulative global solar waste between now and 2050 could reach 60 to 78 million metric tons, assuming a solar panel’s lifespan of 30 years. Yet, IRENA warns that total scrap could reach more than 200 million tons by then.

Additionally, there are many cases where systems are upgraded with new technology 10 to 15 years into their lifespans. Decommissioned panels that aren’t at end-of-life may be suited for reuse. If a used panel is in mint condition, it degrades at an average rate of 0.5 percent per year. At this rate, a 20-year-old panel would still yield 90 percent of the electricity it produced in its first year of operation.

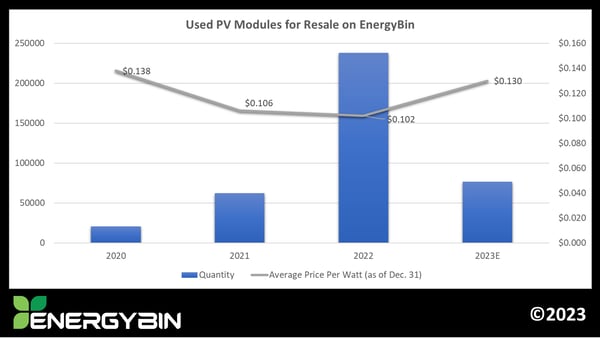

This scenario alone should justify reuse. But the resale market has yet to surge. On EnergyBin, used solar panels currently comprise just 4 percent of the total panels for resale, down from 9 percent in 2022.

The main reason for the decline is the falling price of new panels. At an average price of $0.15-0.20/Wp, buyers get more bang for their buck with new panels.

However, reuse is still viable and necessary for maintenance purposes. Plus, when prices for new panels rise, used panels may become more attractive to bargain buyers throughout the world.

Furthermore, the cost to recycle solar panels today is expensive. The current price ranges from $15-$30 per panel, and the value of raw materials extracted doesn’t cancel out the cost. Of the aluminum, copper, glass, lead, silver, and tin removed during the recycling process, the return amounts to between $2 and $4 per panel.

Policies, subsidies, and incentives would help advance reuse and recycling. These two facets are crucial to achieve a sustainable circular economy. And quite frankly, reuse and recycling are the only responsible ways to manage decommissioned panels. Everything else adds to the global waste problem.

Three major developments achieved this year in the reuse and recycling sectors are worth mentioning. First, as more solar consumers, especially businesses and corporations, clearly define their environmental, social, and governance (ESG) goals with clean energy clauses, we’re seeing an increase in end-of-life management plans included in initial project contracts.

Second, international standards for reuse and recycling are underway. Sustainable Electronics Recycling International (SERI) is in the process of finalizing its R2v3 standard to include solar panels. Solar companies and recycling facilities will soon be able to apply for R2v3 certification, which will help to establish a framework for the secondary market and ease buyers’ concerns regarding the quality and safety of used modules.

Third, several large investments have been made to support infrastructure development and to scale recycling processes. In Grenoble, Europe, ROSI Corporation opened the first high-purity recycling facility last July. This plant is part of a future global network that will expand to other European countries, China, Japan, and the United States.

In the U.S., SOLARCYCLE, Inc., based in Texas, has raised $37 million since its inception in 2022 to scale its recycling capacity and expand materials remanufacturing capabilities. The company also received a research grant from the U.S. Department of Energy for $1.5 million to study the recovery process of high-quality metals and materials.

And in Japan, Marubeni and Hamada launched Rexia Corporation to advance reuse and recycling services throughout the south-east Asian region. Marubeni is also making great strides in deploying blockchain technology to identify and track solar panel lifecycles, which will aid in accurately determining those panels that should be reused rather than recycled.

These developments will pave the way for a robust secondary market. But we’re likely years away from a thriving market in which reuse and recycling are viable options. Even so, today’s investments will reap the economic benefits that the future has in store.

Insights for your business

As we head into 2024, the solar panel market will continue to ebb and flow. The three market conditions addressed in this article – a massive increase in domestic manufacturing, the rise of new cell technology, and the state of reuse & recycling – hold insights for every PV professional.

For manufacturers, know your prices through and through. Buyers want high quality panels, but they also don’t want to overpay. Gain efficiency without sacrificing quality.

Distributors and suppliers should also keep tabs on margins to maintain competitive prices. Additionally, pay attention to where the market is headed in terms of technology. As n-type panels gain market share, don’t get stuck with p-type modules that your primary customers aren’t buying. Now is the time to resell excess stock in the secondary market.

Furthermore, manufacturers, distributors, and suppliers should consider how you can contribute to a robust and sustainable secondary market. Expand customer care programs for existing PV systems by establishing in-house repair departments. Create buy-back programs where customers can turn in reusable components that can then be remarketed. Partner with recycling facilities to ensure decommissioned panels don’t end up in landfills.

For developers, EPCs, installers, and O&M managers, do your pricing research. Overpaying for panels can lead to project delays and cancellations. If you have the warehouse space, you may be tempted to stock up on panels at all-time low prices. To exercise this strategy, keep in mind that buyers are generally looking for higher efficiencies of 20.5 to 21 percent or more. Plus, supply chain challenges are still causing backlogs. Be careful that this strategy doesn’t backfire, leaving you with more panels than you can deploy in a reasonable turnaround time.

If your buy-low strategy fails, and you end up with excess panels, list them for resale in the secondary market to avoid large holding fees. EnergyBin offers a seamless way for PV professionals to buy and sell panels and other hardware. Such a platform also provides a source for locating replacement parts to service existing PV systems.

As your customers turn to you for PV lifecycle assistance, you’ll want to have a plan in place for maintenance, upgrades, and decommissions. Keep in mind that not all decommissioned material is at its end-of-life. Create value-added services for inspection, testing, remarketing, and recycling. Or form a partnership with a secondary market solutions provider who can fulfill your customers’ downstream needs. Have a plan that guarantees responsible sustainability.

More Resources

A Comprehensive Guide to Wholesale Solar Equipment Brokering

A Comprehensive Guide to Wholesale Solar Equipment Brokering

The Ultimate Guide to Buying Wholesale Solar Equipment

The Ultimate Guide to Buying Wholesale Solar Equipment

The Ultimate Guide to Selling Wholesale Solar Equipment

The Ultimate Guide to Selling Wholesale Solar Equipment